|

|

ParaMonte MATLAB 3.0.0

Parallel Monte Carlo and Machine Learning Library

See the latest version documentation. |

|

|

ParaMonte MATLAB 3.0.0

Parallel Monte Carlo and Machine Learning Library

See the latest version documentation. |

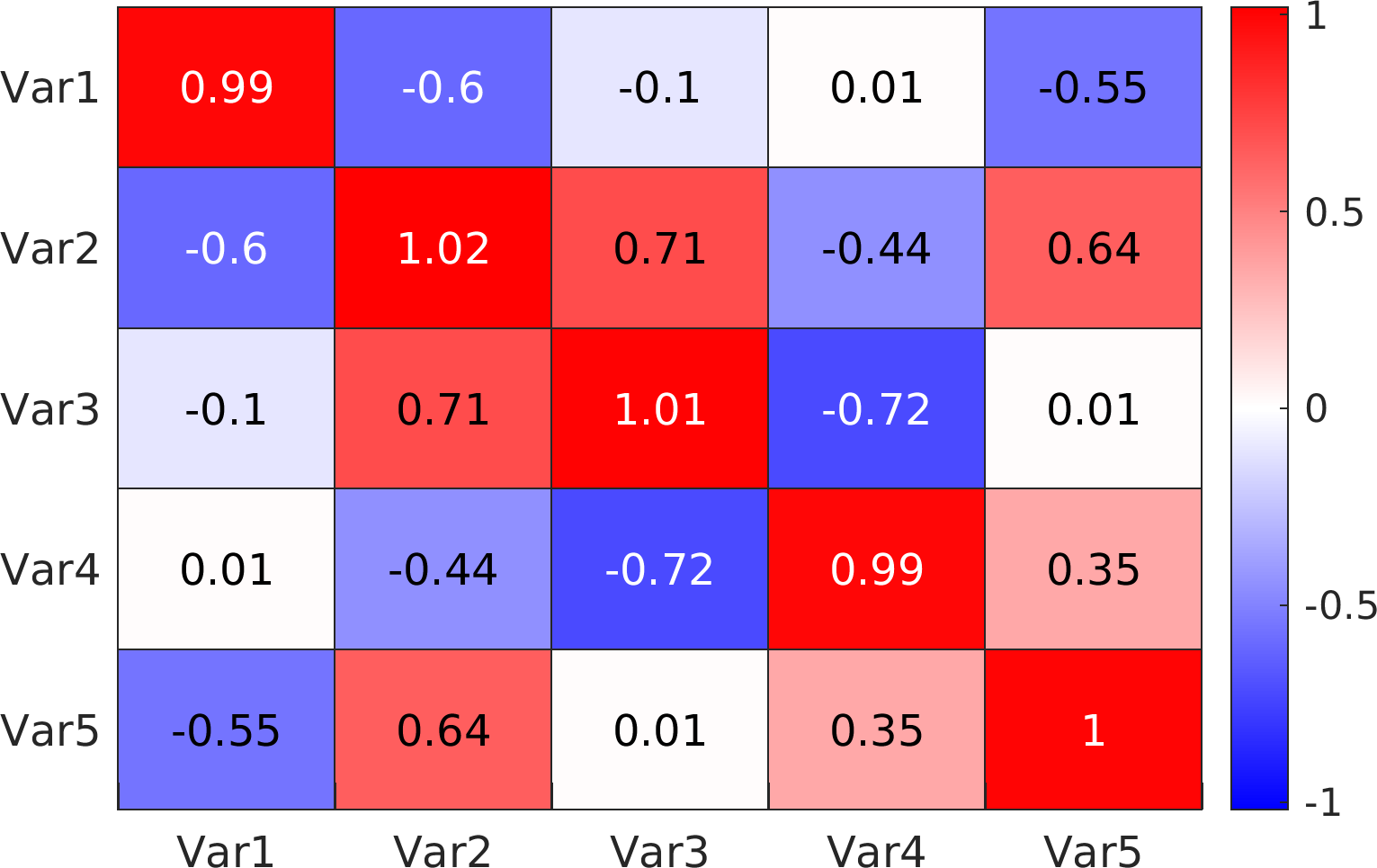

This is the base class for generating objects with methods and storage components for computing and storing and visualizing the covariance matrix of an input data.

More...

Public Member Functions | |

| function | Cov (in dfref, in method) |

| Return an object of class pm.stats.Cov. More... | |

| function | get (in self, in dfref, in method) |

| Return the covariance matrix of the input data. More... | |

| function | setvis (in self, in val) |

| Set up the visualization tools of the covariance matrix. More... | |

Data Fields | |

| Property | dfref |

| Property | method |

| Property | val |

| Property | vis |

This is the base class for generating objects with methods and storage components for computing and storing and visualizing the covariance matrix of an input data.

This is merely a convenience class for easy computation of covariance and its storage all in one place.

The primary advantage of this class over the MATLAB intrinsic functions is in the ability of this class to compute the result for input dataframe table and return the results always in MATLAB table format.

Final Remarks ⛓

If you believe this algorithm or its documentation can be improved, we appreciate your contribution and help to edit this page's documentation and source file on GitHub.

For details on the naming abbreviations, see this page.

For details on the naming conventions, see this page.

This software is distributed under the MIT license with additional terms outlined below.

This software is available to the public under a highly permissive license.

Help us justify its continued development and maintenance by acknowledging its benefit to society, distributing it, and contributing to it.

| function Cov::Cov | ( | in | dfref, |

| in | method | ||

| ) |

Return an object of class pm.stats.Cov.

This is the constructor of the pm.stats.Cov class.

| [in] | dfref | : The input MATLAB matrix or table of rank 2 containing the data as ncol columns of nrow observations whose covariance matrix must be computed.Ideally, the user would want to pass a reference to a dataframe (e.g., as a function handle @()df) so that the data remains dynamically up-to-date.(optional. If missing or empty, the covariance matrix will not be computed.) |

| [in] | method | : The input scalar MATLAB string that can be either:

"pearson") |

self : The output object of class pm.stats.Cov.

Possible calling interfaces ⛓

Example usage ⛓

Final Remarks ⛓

If you believe this algorithm or its documentation can be improved, we appreciate your contribution and help to edit this page's documentation and source file on GitHub.

For details on the naming abbreviations, see this page.

For details on the naming conventions, see this page.

This software is distributed under the MIT license with additional terms outlined below.

This software is available to the public under a highly permissive license.

Help us justify its continued development and maintenance by acknowledging its benefit to society, distributing it, and contributing to it.

| function Cov::get | ( | in | self, |

| in | dfref, | ||

| in | method | ||

| ) |

Return the covariance matrix of the input data.

This is a dynamic method of the pm.stats.Cov class.

This method automatically stores any input information in the corresponding components of the parent object.

However, any components of the parent object corresponding to the output of this method must be set explicitly manually.

| [in,out] | self | : The implicitly-passed input argument representing the parent object of the method. |

| [in] | dfref | : The input (reference to a function handle returning a) MATLAB matrix or table of rank 2 containing the ncol columns of nrow data whose covariance matrix must be computed.Ideally, the user would want to pass a reference to a dataframe (e.g., as a function handle @()df) so that the data remains dynamically up-to-date.(optional. If missing, the contents of the corresponding internal component of the parent object will be used.) |

| [in] | method | : The input scalar MATLAB string that can be either:

"pearson") |

val : The output MATLAB table containing the covariance matrix.

Possible calling interfaces ⛓

Final Remarks ⛓

If you believe this algorithm or its documentation can be improved, we appreciate your contribution and help to edit this page's documentation and source file on GitHub.

For details on the naming abbreviations, see this page.

For details on the naming conventions, see this page.

This software is distributed under the MIT license with additional terms outlined below.

This software is available to the public under a highly permissive license.

Help us justify its continued development and maintenance by acknowledging its benefit to society, distributing it, and contributing to it.

| function Cov::setvis | ( | in | self, |

| in | val | ||

| ) |

Set up the visualization tools of the covariance matrix.

This is a dynamic Hidden method of the pm.stats.Cov class.

This method is inaccessible to the end users of the ParaMonte MATLAB library.

| [in,out] | self | : The implicitly-passed input argument representing the parent object of the method. |

| [in] | val | : The input (reference to a function handle returning a) MATLAB matrix or table of rank 2 containing the computed covariance matrix to be visualized.Ideally, the user would want to pass a reference to a dataframe (e.g., as a function handle @()df) so that the data remains dynamically up-to-date.(optional. If missing, the contents of the corresponding var attribute of the parent object will be used.) |

Possible calling interfaces ⛓

Final Remarks ⛓

If you believe this algorithm or its documentation can be improved, we appreciate your contribution and help to edit this page's documentation and source file on GitHub.

For details on the naming abbreviations, see this page.

For details on the naming conventions, see this page.

This software is distributed under the MIT license with additional terms outlined below.

This software is available to the public under a highly permissive license.

Help us justify its continued development and maintenance by acknowledging its benefit to society, distributing it, and contributing to it.

| Property Cov::dfref |

dfref

A scalar object of class pm.container.DataFrame containing the user-specified data whose covariance must be computed.

| Property Cov::method |

method

The scalar MATLAB string containing the method of computing the covariance matrix.

It can be either:

"pearson" : for computing the Pearson covariance matrix of the input data."spearman" : for computing the Spearman rank covariance matrix of the input data.| Property Cov::val |

val

The MATLAB table of rank 2 serving as a convenient storage component for the covariance matrix.

This component is automatically populated at the time of constructing an object of class pm.stats.Cov.

It must be populated manually at all other times.

| Property Cov::vis |